How to Treat the Hugely Endowed

Studies show that the well endowed are good for society.

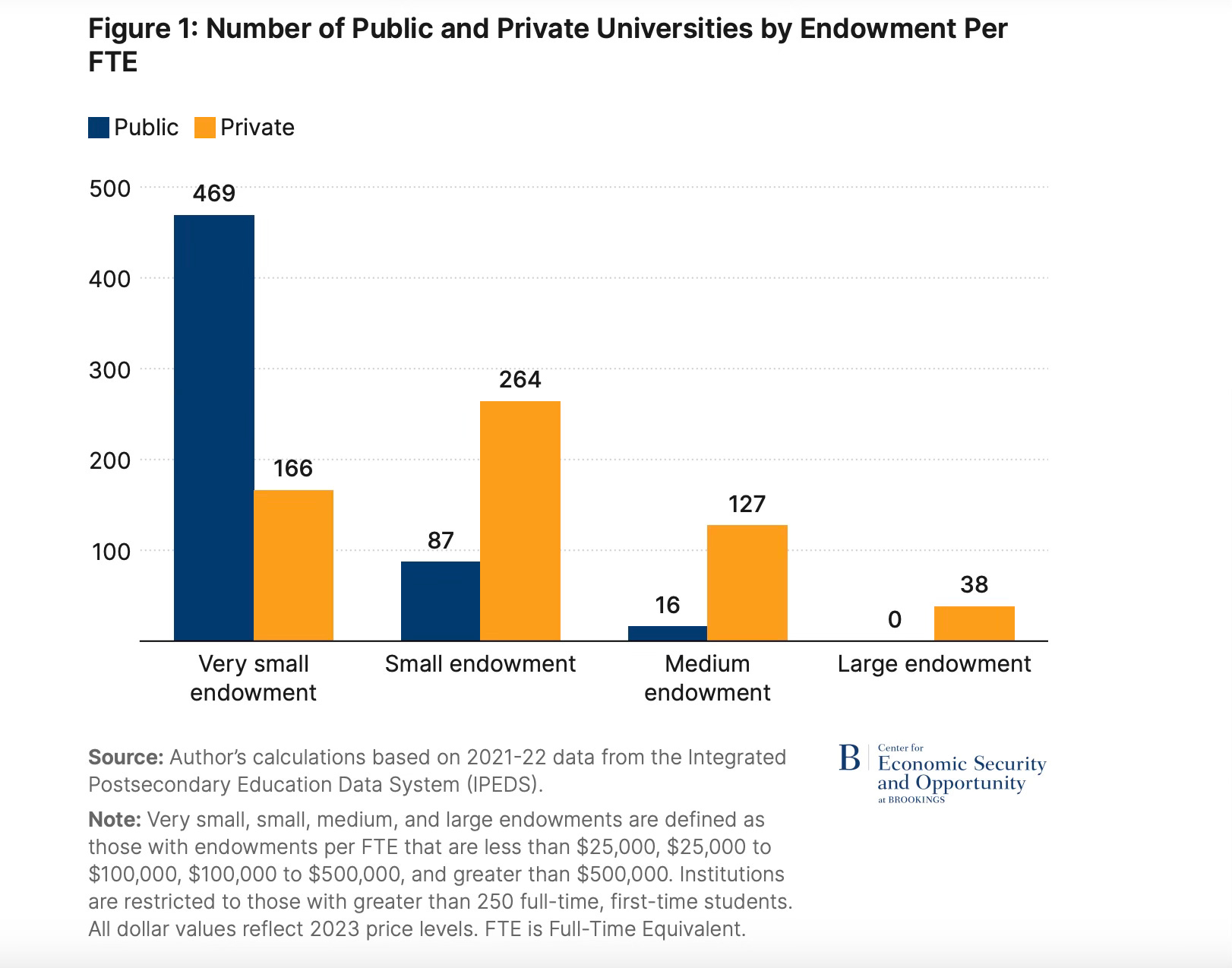

A handful of universities have massive endowments, on the order of the gross domestic products of some nations. Harvard University’s endowment tops $50 billion, which is close to the entire annual economic output of Jordan. The universities with the largest endowments, and which are able to spend the most on each of its full time enrolled students, are all private. Public universities tend to have very small endowments, or none at all. They rely almost entirely on tax subsidies and tuition to cover expenses.

This has important implications for social mobility wealth concentration in the United States and around the world. Phillip Levine at Brookings wonders if the massive concentration of wealth at a few private and highly selective schools is a problem best solved through taxation and redistribution. His conclusion? Not exactly, but universities with big endowments need to do a better job at using that money to create widespread benefits for society.

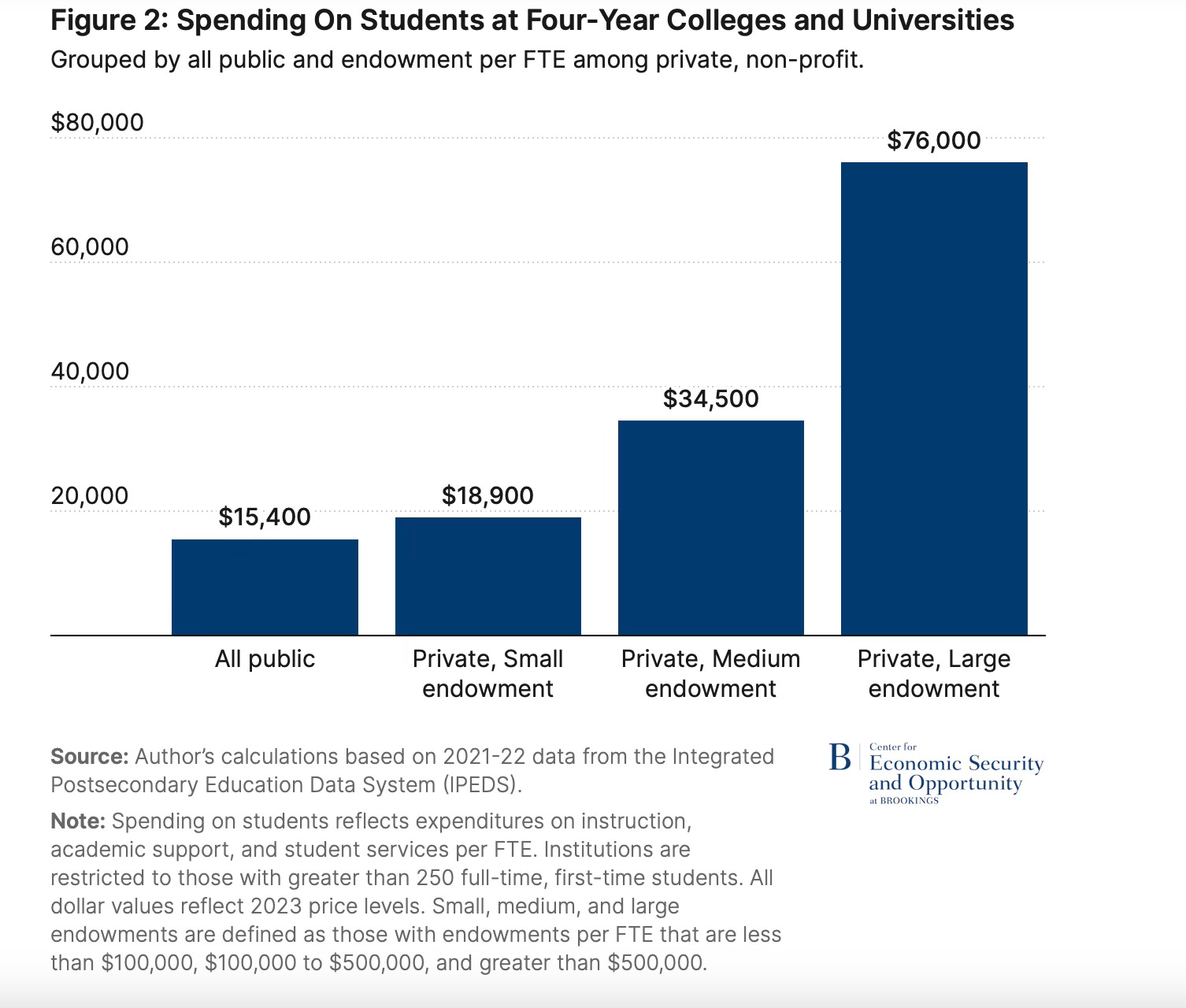

First, let’s look at the problem, which Levine captures well in a pair of charts:

The concentration of large endowments at just a few universities creates massive disparities in spending per student:

It’s worth noting (and Levine does) that the United States now modestly taxes universities with very large endowments, described as having more than $500,000 in assets per full time student. The 1.4% tax was part of the Bipartisan Budget Act of 2018 and probably has trustees of the University of Pennsylvania’s $21 billion endowment shaking their heads over letting Donald Trump walk around with a degree from Wharton.

If you can, and I don’t blame you if you refuse this big ask, try not to pull out the world’s tiniest violin of sympathy when I said that dealing with a huge endowment is hard. The people entrusted to manage these portfolios have to meet both the present and future needs of the school. The mandate is to create intergenerational equity so that the school is as equipped to serve its students 50 years from now as it is today.

To do that, money managers have to generate “equity like returns,” which would come in around 8% per year, without taking on all of the risk of owning equities or even a 60/40% stock and fixed income portfolio. That means diversifying among a lot of different asset classes like equipment leases, pharmaceutical royalties, owning music catalogues or farmland in Africa. The mission is to build a portfolio of assets that can get you to that 8% return with low enough volatility that the money is there when the school needs it, even if economic times are sour. A big endowment always has to be ready to go, after all.

So, that 1.4% tax might seem modest, but when you’re competing with others to invest in the assets that will generate that 8% return that little seeming tax can become a big hurdle. It is 17.5% of the return the endowment needs to meet its present and future demands. So what seems small from outside is a big problem for the people running the money.

Levine believes that if they make their target returns, college endowments can spend between 3-4.5% of assets every year. This is actually a good deal less than the typical 5% spending target for charitable foundations. The result is, says Levine, that even the richest schools have to make tough choices, including between spending on facilities, research programs, faculty or focusing on financial aid. Levine believes that the financial aid focus, if well-targeted to help students from lower earning households, is the best argument against taxing endowments.

Levine sums up the access vs. program spending well:

“Both goals cost money. Striving for excellence is expensive. Offering affordable pricing has an opportunity cost. Ultimately, excellence and access are both important goals that need to be delicately balanced.

Both public and private institutions face this trade-off, but they are likely to weigh the factors differently. Access is a core part of the mission at public institutions: they are funded by states to educate the populace at large, not just the wealthy. Private institutions value access as well, but it is less fundamental to their existence. One may not expect enrollment rates of lower- and middle-income students at these private institutions to match those at public institutions.”

The good news, he says, is that these private institutions really are investing in access for lower income students but that the number of people they actually reach is still small relative to the population.

Working class young people are more likely to attend public universities, which don’t have large endowments or, most often, any endowments at all. Endowment size is, however, directly related to how much an institution spends on its students, which may not be delta-1 to quality of education but is a pretty good barometer.

That means, of course, that the investment a select private institution will make in its students is much larger and more consequential than the investment a small private or large public institution can make. This might be the best argument for increasing taxation of private university endowments, if the proceeds from those taxes are re-distributed to endow public and smaller private universities. It might well be, after all, that public university graduates can do a lot more for society, if we invest more in them. Getting working class people into elite universities is great and all, but making the universities that actually serve most of the population better seems like a superior allocation of resources.

I think an endowment manager would, grudgingly, have to agree. It’s not the size, after all, but how you use it that counts.