Middlebrow Takes on the Economy

Why is everything so weird?

After the Financial Crisis, Mohamed El-Erian, then chief investment officer of PIMCO alongside fixed income manager Bill Gross, coined the phrase “new normal” to describe low growth conditions that would lead to rising wealth inequality that persisted for years. The PIMCO call was correct and the post-Crisis recovery could be considered a separate era from the long boom that emerged at the end of the high inflation period of the 1970s. The slow growth era endured until the start of the pandemic, punctuated by the debt ceiling war of 2011, the Euro Zone sovereign debt crisis and finally the U.S. Federal Reserve tapering quantitative easing and starting to raise interest rates. Rates never reached normalized level as inflation remained subdued and the coronavirus upended further economic planning.

After the short but sharp pandemic recession, a “new normal” has not emerged for the late-pandemic era. Investment adviser Barry Ritholtz dubs this “The Post Normal Economy.” So many of his preferred metrics, he says, are not behaving as they did historically. Writes Ritholtz:

….Most economic data is merely a continuation of prior trends and therefore not all that important.

But as I run through all of my market and economic charts, I am continually reminded just how abnormal this economic cycle is.

Look at the red line on the employment chart (top): We had the fastest, deepest payrolls collapse in the post-war period, followed by the strongest ever recovery.

¯\_(ツ)_/¯

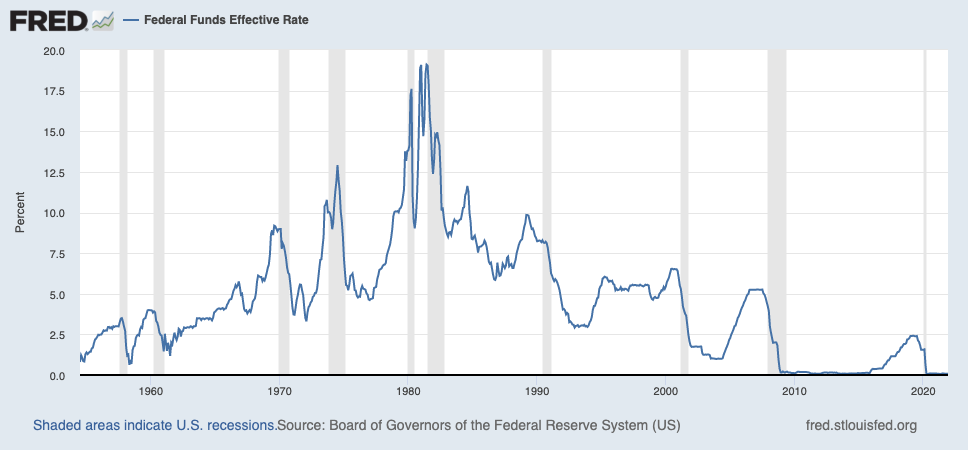

Ritholtz argues that in the face of such strangeness, we should all be careful about the economic and market commentaries we consume — most forecasts are based on history that might not apply to current events. Middlebrow has consumed a lot of conventional economic and market wisdom of late. Two big arguments have been that the Federal Reserve will reduce its balance sheet and raise interest rates, causing massive corrections for equities (particularly growth stocks) and real estate (which is generally financed with debt that will become more expensive). As rates rise, goes the story, cash will turn king as risk free savings account resume interest payments. This is all very conventional wisdom, based on this chart:

There’s always somebody saying, “It’s different this time,” and they are generally wrong. But Ritholtz, a truly honest broker and a data-driven thinker, is not cavalier about saying we’re in unprecedented circumstances. Multiple indicators, from employment to savings rates to consumption are behaving ahistorically. Nobody can say how long strange conditions will persist, but that doesn’t mean they don’t exist.

When it comes to investing, professionals all have their own ideas and philosophies. Covering and working in financial services for two decades has taught me that almost all of these approaches have some merit, when properly applied. Value and growth investment strategies can both work. Prvate equity is great, if you can afford it. Hedge funds can be fabulous. Academic research even supports things that seem like (technical analysis, or chart reading, actually does seem to encode fundamental insights over short time horizons).

Never lecture people if an idea that doesn’t appeal to you like crypto or NFTs does appeal to them. They might know what they’re doing and why. People who claim that the stock market is unbeatable over lengths of time, that investment performance is mean reverting and that everybody should index have a point. But Middlebrow has met and worked with many long-term winners, so the argument for indexing is a great rule of thumb that is made to be broken (like, um, a thumb).

Most economic commentators and investment managers adhere to lessons of history because it’s the only reliable tool for decision-making. They also use historic data to validate and promote their investment ideas, methods and philosophies. The marketing guidelines demand that every description contain the disclaimer that past performance doesn’t guaranty future success, but there are really only two ways to evaluate an investment or forecasting strategy:

Track record.

An independent analysis of the reasoning behind the approach and an evaluation of its chances for success in prevailing conditions.

That’s it. You either put your faith in bygone success or decide, based on evidence and logic, that the approach seems reasonable under the circumstances.

As for the professionals, well, most of them stick to one way of doing things in all conditions because it’s the best way to stay sane and because investment clients value knowing how their manager will act over time. Middlebrow remembers a value mansger with billions under his oversight, once told me that sticking to a strict philosophy of buying well-capitalized companies trading below his estimate of fair value was more than just a method he believed would be effective but an ethos that he could follow when decision-making became difficult. Market nihilism would have rendered him a wavering Hamlet.

Middlebrow prefers the term “political economy” to “economics,” because economics can’t be separated from human decisionmaking and deliberation. It’s difficult to imagine the political reaction to persistent inflation, which we have not experienced since the start of the long global economic boom in the 1980s. Almost no decisionmakers Gen-X or younger have any sense of what persistent inflation and rising rates would be like.

On the other hand, there’s a reason for that — the twin deflationary engines of technology and globalization have, for four decades, quashed first world inflation before it can take hold. Has technological progress peaked? Is globalization over? Is a broken supply chain really a permanent obstacle to a world empowered by supposedly wondrous machine learning and AI technologies?

For what it’s worth (Ritholtz would say nothing, and Middlebrow agrees) it seems like this period of weirdness might be an interregnum — a pause between the end of one era and the start of the next.

That’s not particularly useful because, who can say what’s coming next? For what it’s worth (and this is a free newsletter) Middlebrow suspects short-term volatility but an emergent long boom driven by increasing technological efficiency with biotecnology proving pivotal and transformative, driven by next generation networks and computing power advances introduced during the pandemic.